The weak yen still matters: what currency moves mean for Japan property investors

For overseas investors looking at Japanese real estate, the yen remains one of the most important parts of the story.

That is not new. For the past several years, currency has been one of the clearest advantages for foreign buyers entering Japan, particularly those bringing capital from the US, Singapore, Hong Kong, the UK, Europe or Australia. What is more striking now is that this advantage has not disappeared—even as global uncertainty has risen sharply.

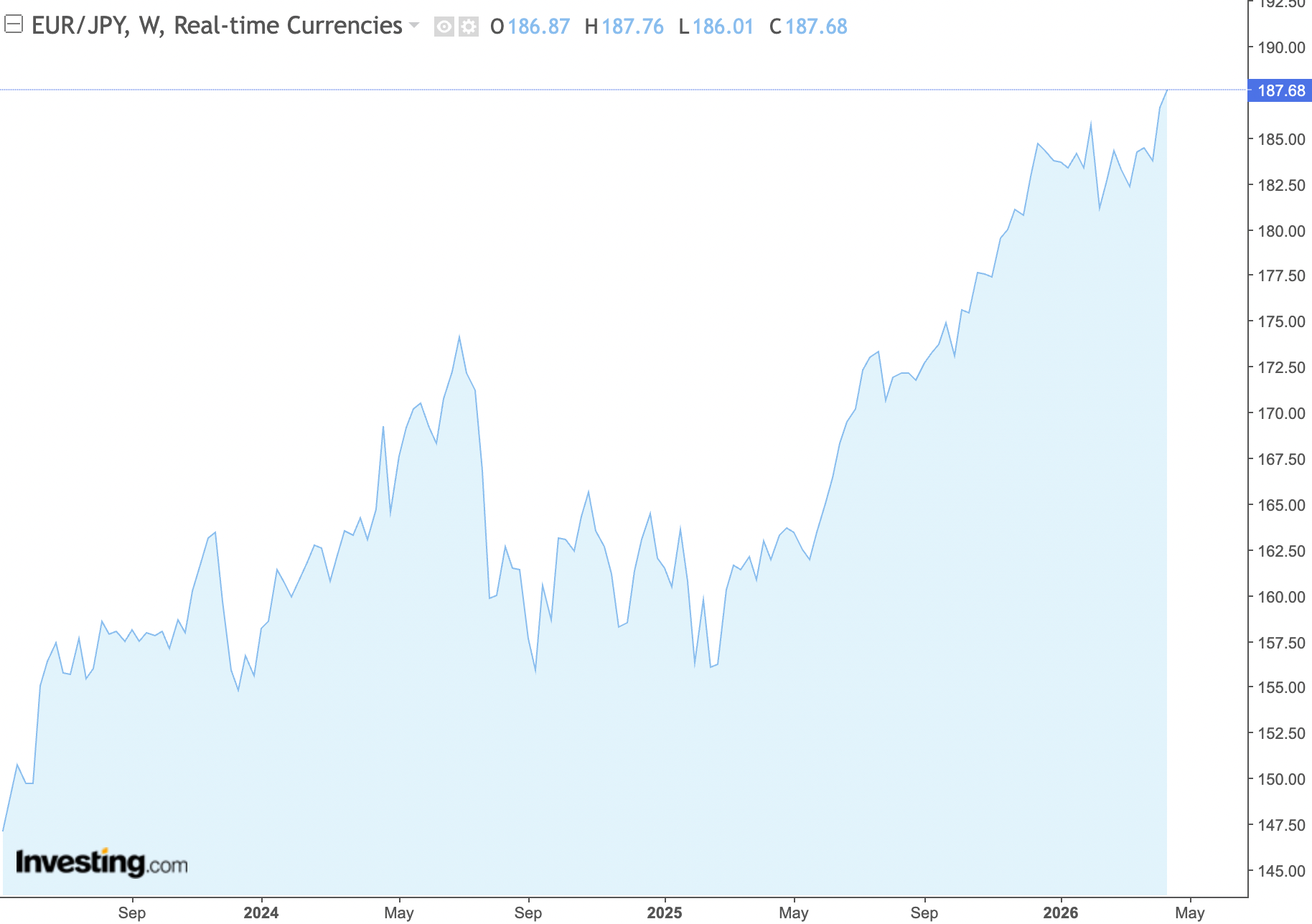

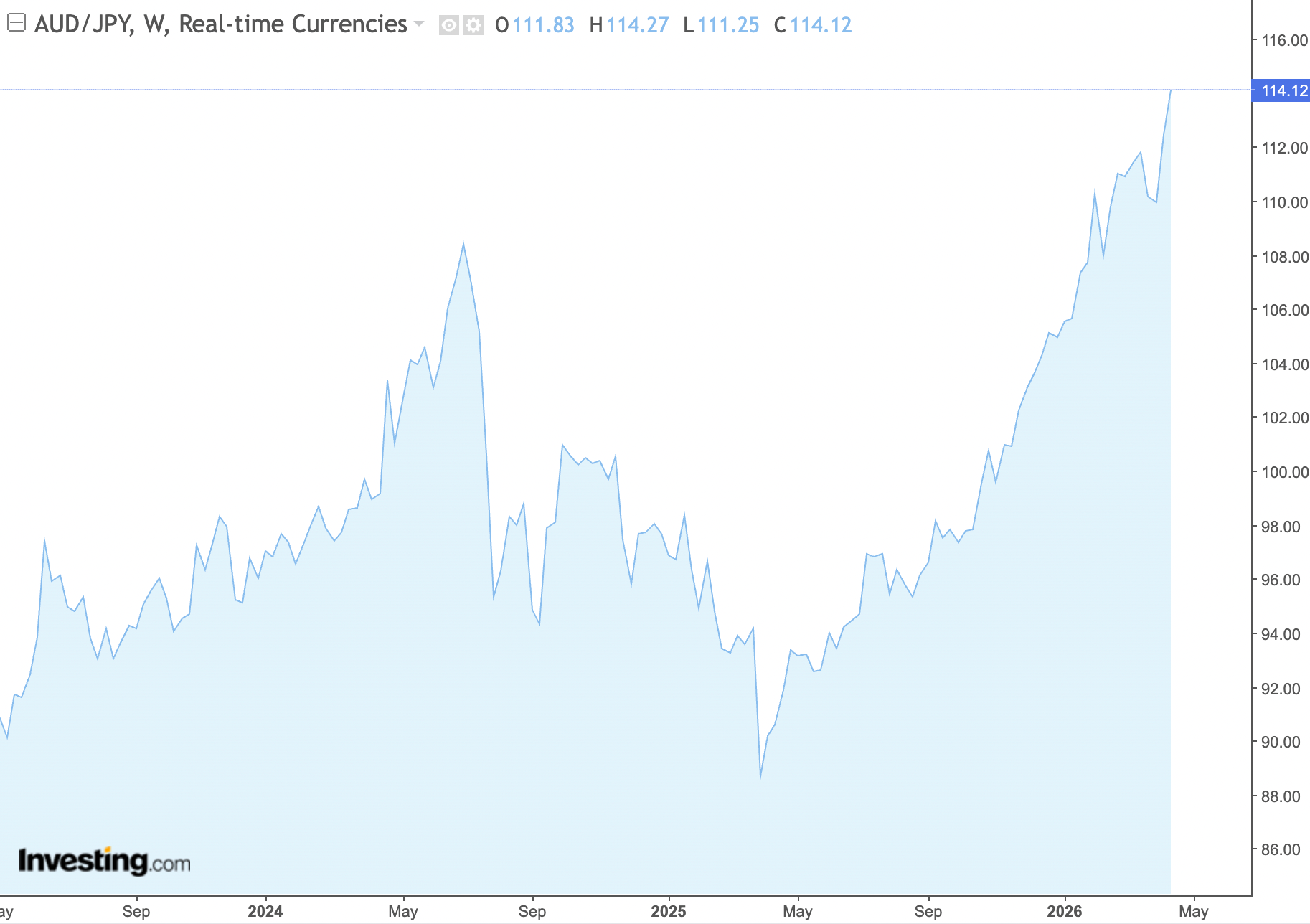

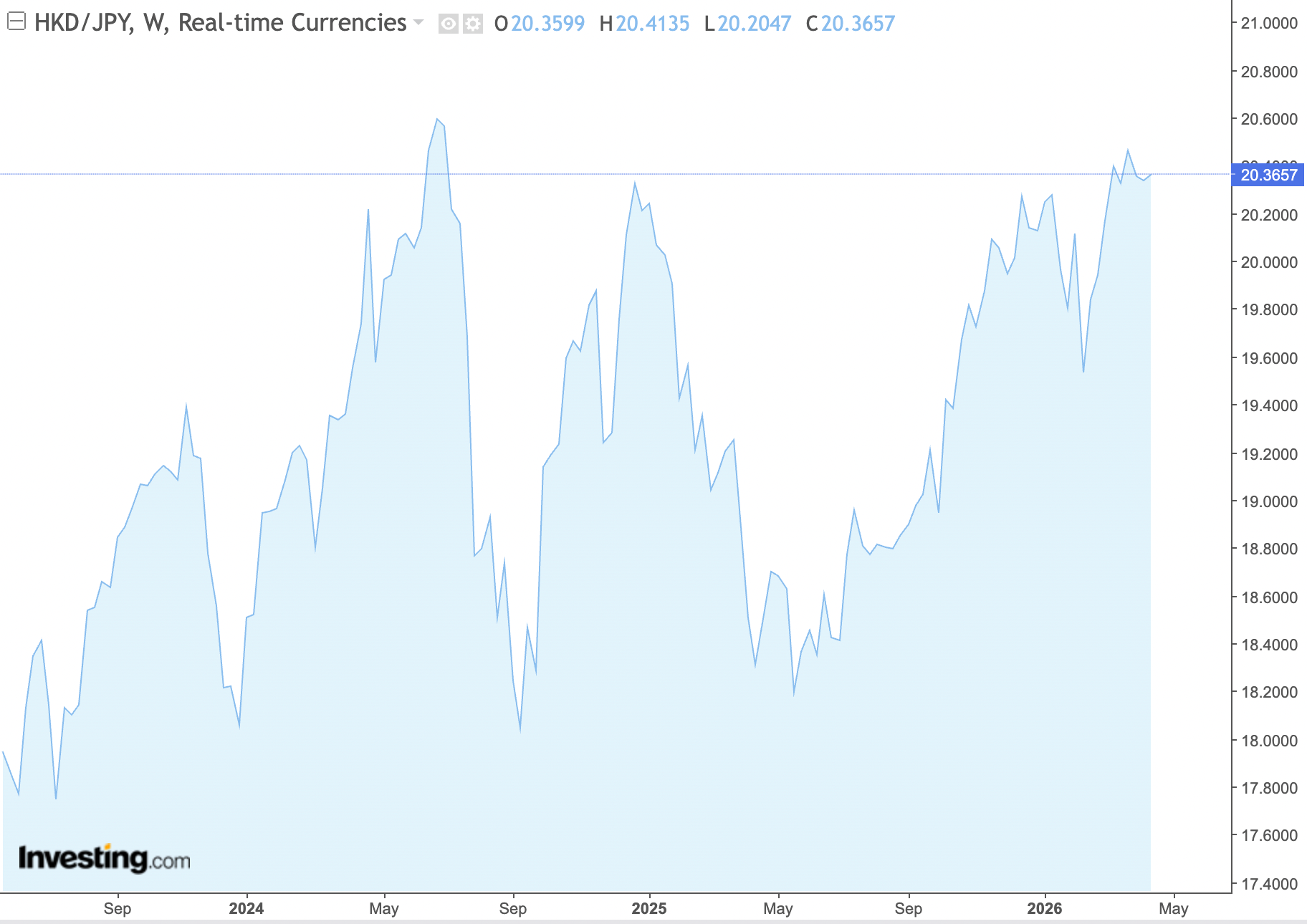

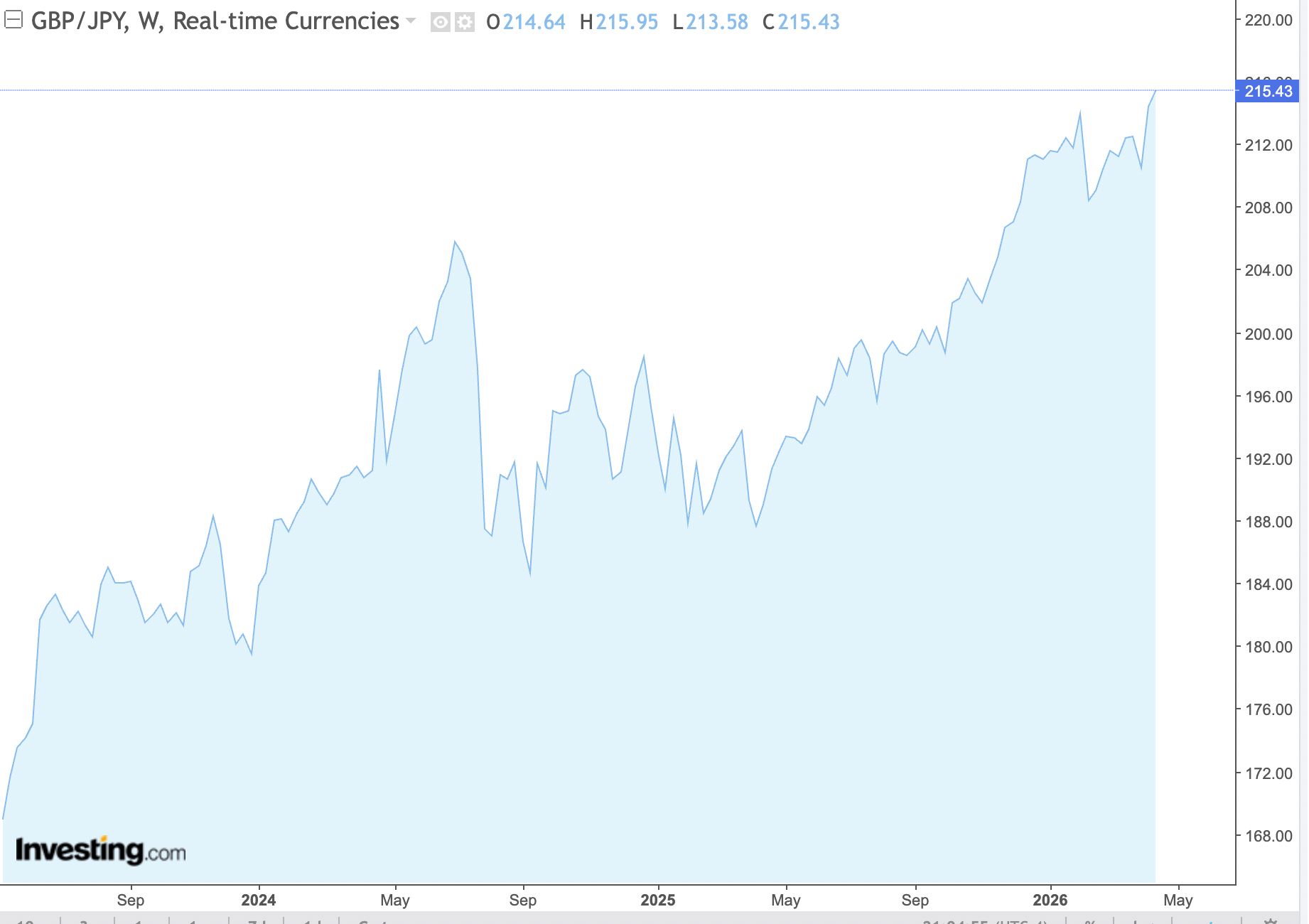

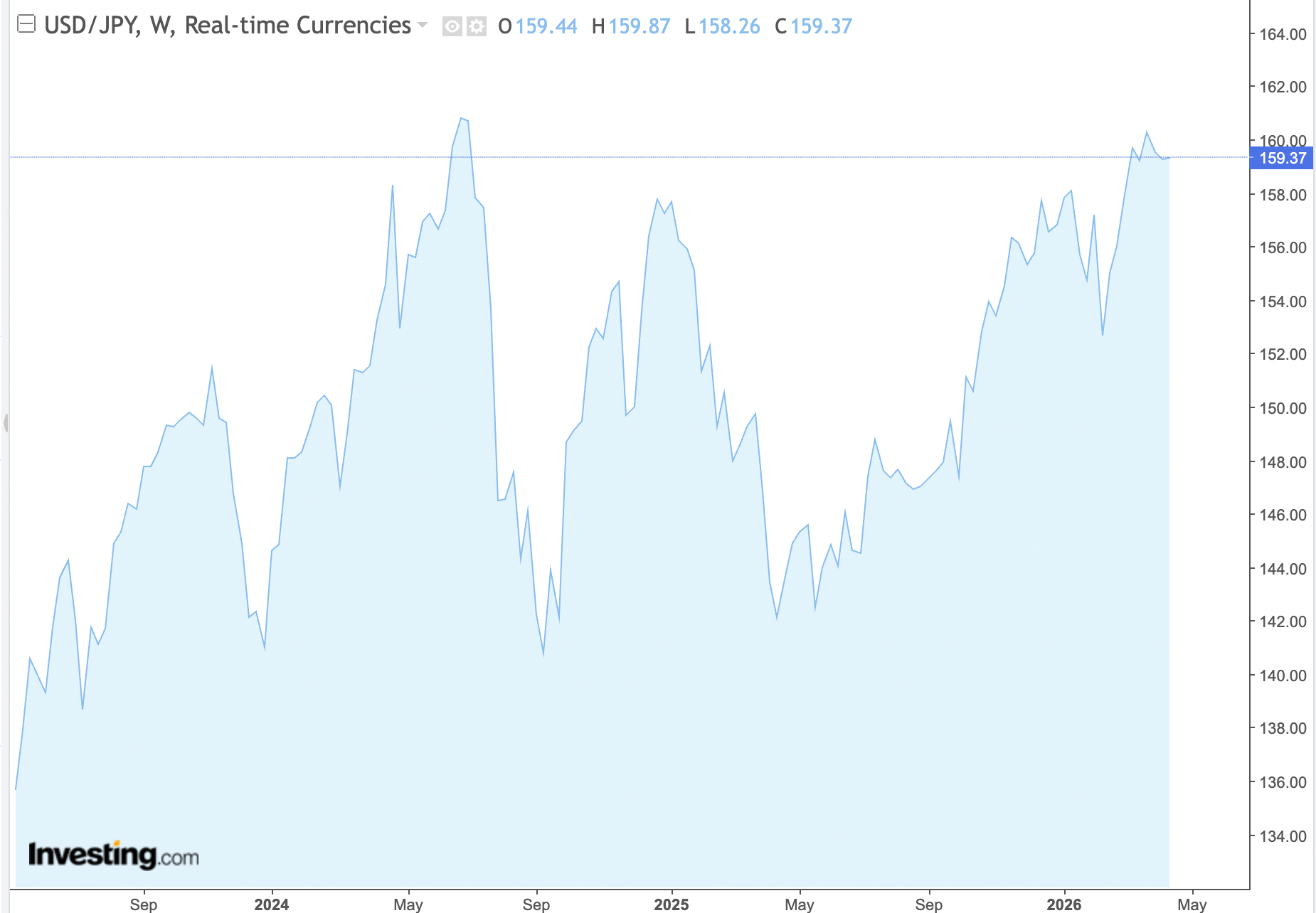

The yen is still trading at roughly ¥159 to the US dollar, ¥125 to the Singapore dollar, ¥20.4 to the Hong Kong dollar, ¥114 to the Australian dollar, ¥215 to sterling and nearly ¥188 to the euro. In practical terms, that means Japan remains comparatively cheap in foreign-currency terms for many international buyers, even after several years of asset-price growth in key markets.

For property investors, this matters in two ways. First, a weak yen lowers the entry cost of acquiring Japanese assets. Secondly, it can improve the optics of returns when rents or eventual sale proceeds are translated back into stronger home currencies. Even where local prices have risen, currency has often softened the blow.

That has been particularly important in resort real estate. In markets such as Niseko, Hakuba and increasingly other mountain destinations, buyers are often not thinking in yen first. They are thinking in Singapore dollars, Hong Kong dollars, US dollars, pounds or euros. Seen through that lens, the Japanese property story has remained more attractive than domestic yen pricing alone might suggest.

But currency is never just a bonus. It is also a signal.

Traditionally, the yen was viewed as one of the world’s classic safe-haven currencies. In periods of war, market panic or financial volatility, capital often flowed into Japan. That relationship now looks weaker and less automatic than it once did. Despite conflicts, inflation shocks and broader global uncertainty, the yen has not staged the kind of sustained defensive rally that investors of an earlier era might have expected.

There are several reasons for that. The most obvious is interest-rate differentials. Japan still has much lower rates than most developed markets, even after the Bank of Japan began moving away from the ultra-loose framework that defined the previous era. The BOJ’s policy rate is currently around 0.75%, which is far above where Japan stood a few years ago but still low in international terms. That continues to make the yen less compelling from a yield perspective, particularly when investors can hold other currencies at materially higher rates.

That helps explain why the yen can remain weak even when uncertainty rises. Safe-haven status has not disappeared entirely—but it now competes with a much more practical question from global investors: why hold a low-yielding currency when inflation is no longer negligible and alternative cash returns are higher elsewhere?

That brings us to inflation.

For decades, Japan’s problem was too little inflation. Now it is managing the opposite transition: inflation is no longer absent, but nor is it yet fully entrenched in the way seen in some Western economies. This creates a difficult balance for the government and central bank. The BOJ wants to normalise policy gradually and avoid falling behind the inflation curve, but it also does not want to tighten too aggressively into an economy still vulnerable to external shocks.

That balancing act has become harder because a weak yen itself is inflationary. It raises the local cost of imported energy, food and raw materials. For households, that means a persistent squeeze on living costs. For investors, it means that Japan’s weak-currency advantage cannot be viewed in isolation from the domestic pressures it creates.

The Japanese government’s position reflects that tension. Tokyo is still highly sensitive to consumer pain from inflation, particularly through energy and imported essentials, and remains wary of any sharp rise in borrowing costs. The result is a policy mix that looks cautious on rates and selective on fiscal support. The BOJ has moved away from the emergency settings of the past, but it is still proceeding carefully. The government, meanwhile, appears more focused on cushioning households and preserving stability than on forcing a rapid yen rebound at any cost.

That matters because many overseas investors assume a weak yen is an uncomplicated positive. It is not. It helps with acquisition pricing, but it also points to a Japanese economy that remains exposed to imported inflation and dependent on stable global energy flows.

The Middle East is central to that risk. Japan still relies on the region for the overwhelming majority of its crude oil imports. That means any conflict involving Iran, and any disruption around the Strait of Hormuz in particular, is not a distant geopolitical concern for Japan—it is a direct economic risk. Higher oil prices feed quickly into import costs, transport, utilities and household sentiment. They also complicate monetary policy: the BOJ has to decide whether energy-driven inflation should be treated as a reason to tighten, or as a shock that could weaken growth if policy is tightened too far.

For real estate investors, especially those considering resort assets, this is more important than it may first appear.

A weaker yen can be very supportive for inbound demand. Japan looks cheaper. Travel feels more affordable. Resort property appears better value relative to alpine alternatives in Europe, North America or Australia. That can support transaction activity, especially from foreign lifestyle buyers and long-hold investors.

But if yen weakness is being sustained by the wrong fundamentals—high import dependence, weak domestic purchasing power and geopolitical energy stress—then investors need to be more selective. A weak currency is most constructive when it sits alongside stable growth, credible inflation management and improving local incomes. It is less reassuring when it reflects unresolved structural fragility.

This is why the current moment is so interesting.

For foreign investors, Japan still offers a genuine currency discount. That remains one of the clearest advantages in the market. Yet the macro backdrop is becoming more complex. The BOJ is no longer frozen. Inflation is no longer negligible. Energy risk is no longer abstract. And the yen no longer behaves quite like the old textbook safe haven.

The investment conclusion is not that the currency tailwind has ended. It has not. If anything, the yen still looks unusually weak against several of the currencies most relevant to international property buyers. The more useful conclusion is that currency should now be read not just as an opportunity, but as information.

It tells investors Japan is still cheap in relative terms. It also tells them why.

For those buying quality real estate in strong locations, that may still be an attractive combination. But it is one that now deserves a little more scrutiny than a simple “weak yen equals good value” narrative.